GE Vernova

The world’s grid bottleneck becomes its best business

General Electric spent 132 years building one of the largest industrial conglomerates in history. Larry Culp took roughly five and a half years to break it apart.

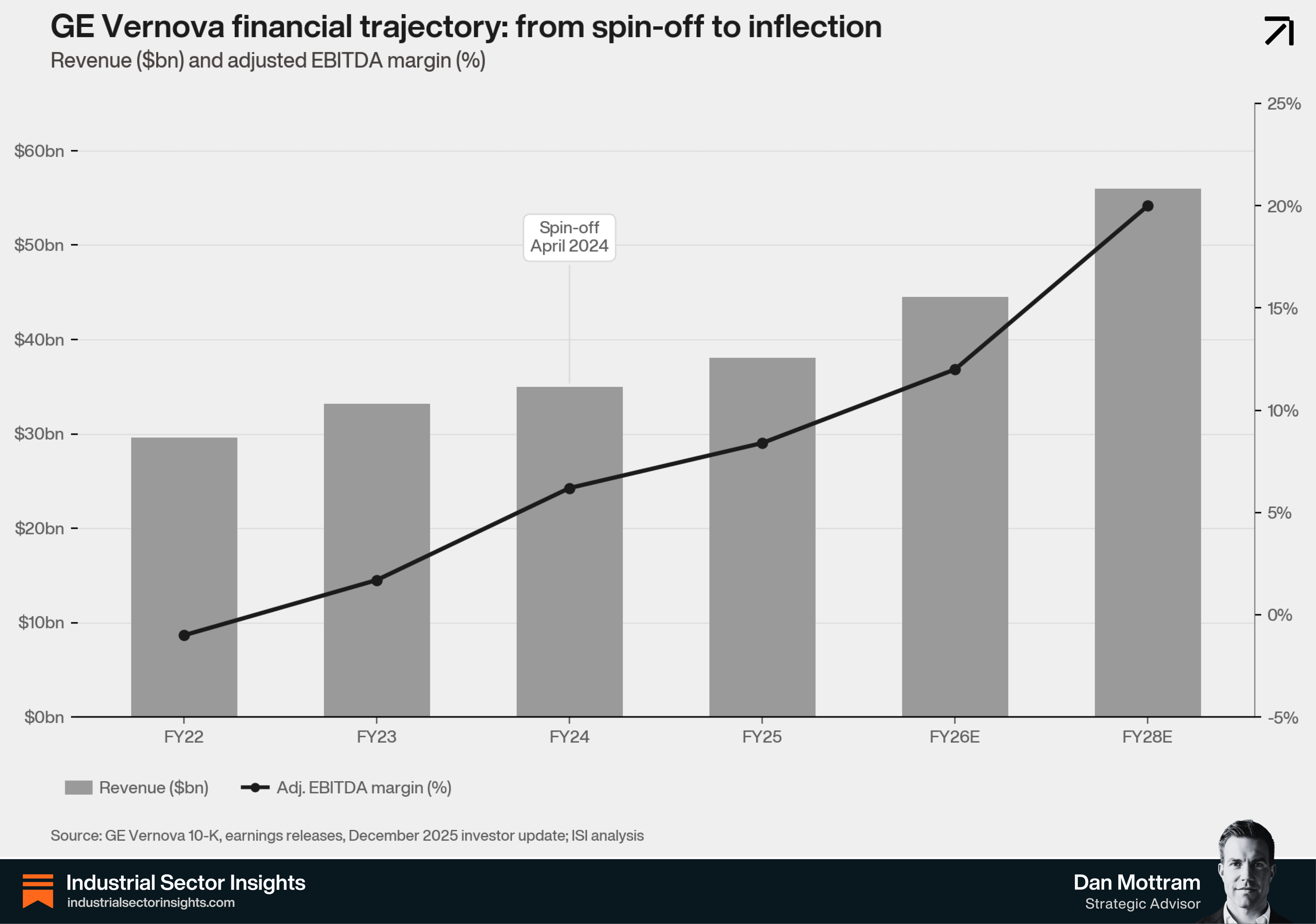

The result, GE Vernova, began trading on the New York Stock Exchange on April 2, 2024, under the ticker GEV. Shares opened at approximately $140 that morning. By February 12, 2026, the stock hit an all-time high of $846, a gain of more than 500 per cent from its opening price in under two years. That performance is harder to explain by pointing at wind turbines and solar panels than most investors initially assumed.

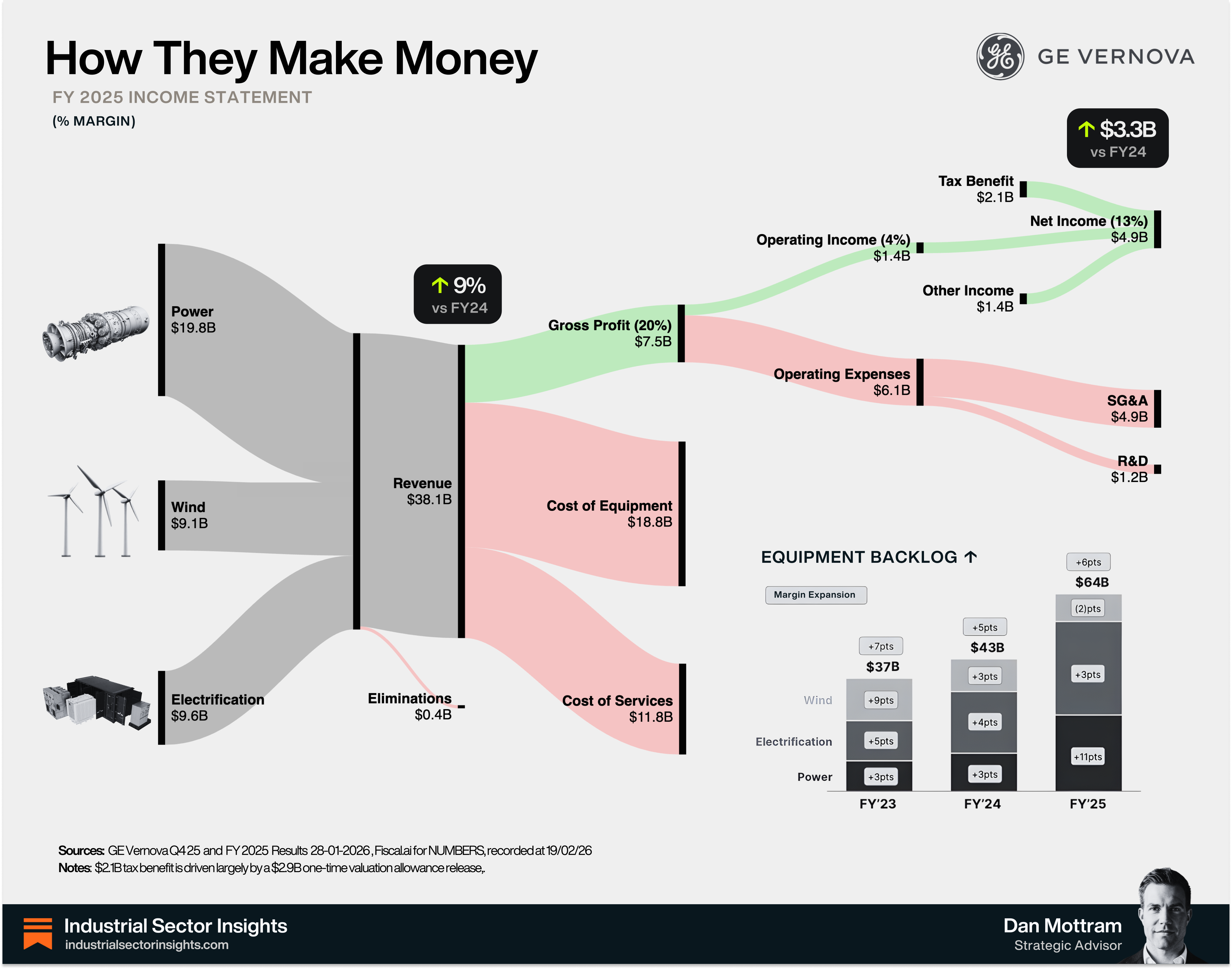

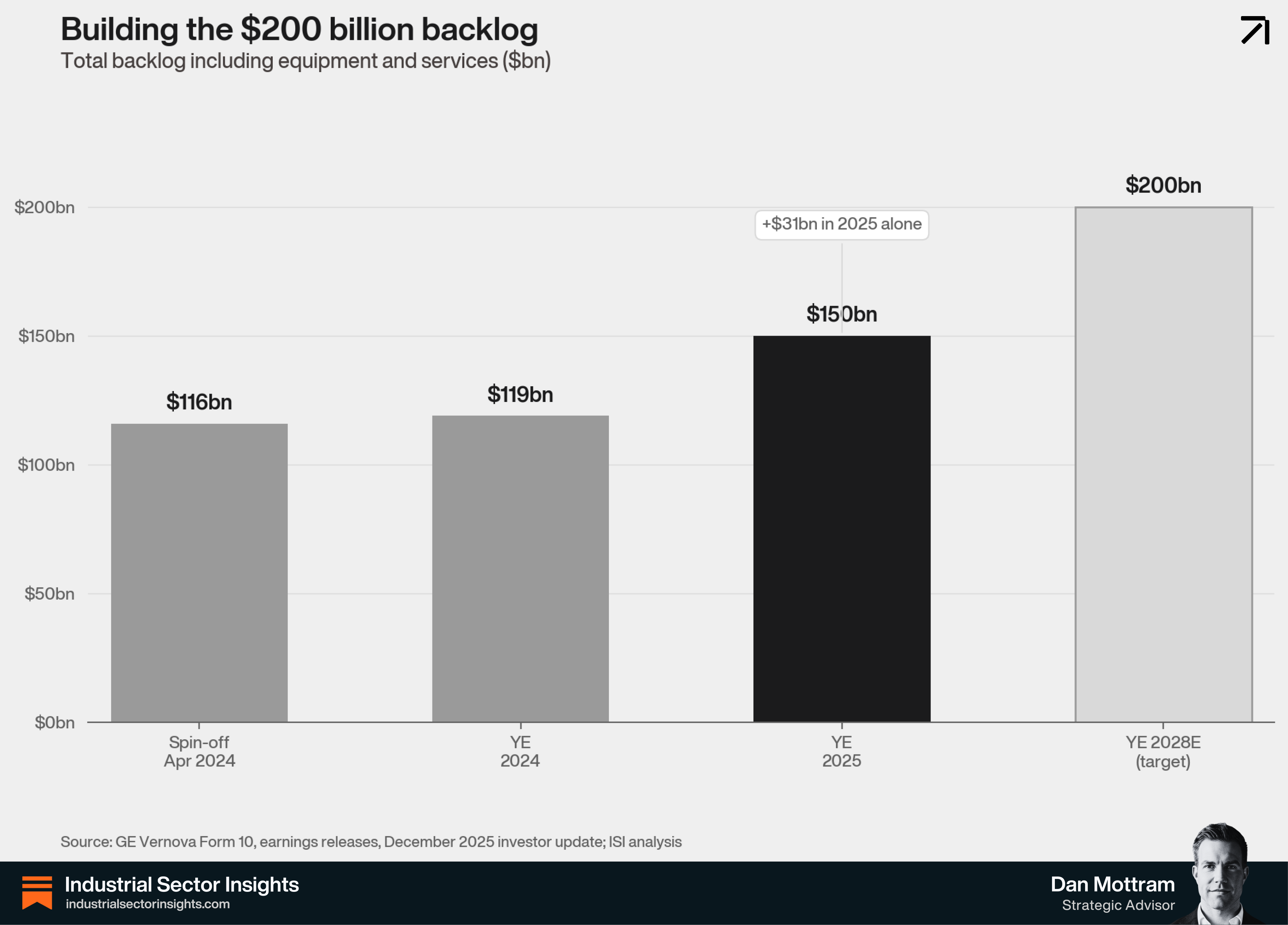

The company generated $38.1 billion in revenue in 2025, up 9 per cent from $35 billion the year before. Its Power segment contributed $19.8 billion, Electrification $9.6 billion, and Wind $9.1 billion. Orders reached $59.3 billion for the year, up 34 per cent organically, building the total backlog to $150 billion by year-end. Gas turbines are driving that order growth. The energy transition narrative often treats them as a sideshow. The financials say otherwise.

Key insights

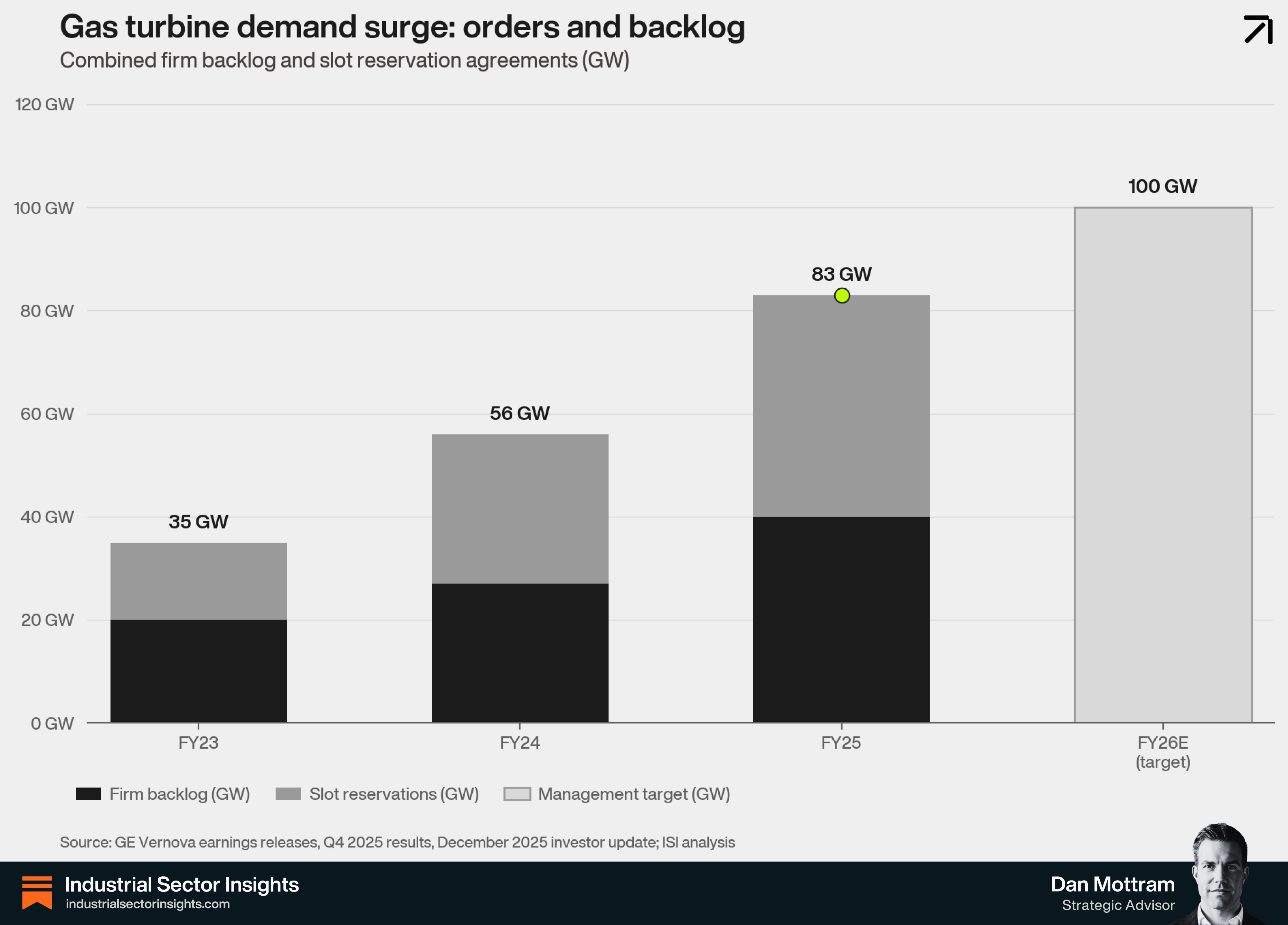

Gas is the growth engine: Power orders hit $32.8 billion in 2025, up 52 per cent organically, with gas turbine backlog reaching 83 GW and management targeting 100 GW by end of 2026.

Electrification is re-rating the stock: Revenue grew 26 per cent to $9.6 billion, with Q4 orders running at 2.5 times revenue, signalling that demand for grid equipment is outpacing supply capacity.

Wind remains the open wound: Segment EBITDA losses hit approximately $600 million in 2025, well above initial guidance, and 2026 will bring further revenue declines and losses of approximately $400 million.

Backlog is the balance sheet: The $150 billion total backlog grew $31.2 billion in 2025 alone, with equipment margins expanding six points year-over-year, meaning new contracts are priced better than the work being delivered.

Execution risk is the variable: The 2028 targets of $56 billion in revenue and 20 per cent EBITDA margin require converting backlog into cash at margins GE Vernova has not yet demonstrated at scale.

How GE got here

The GE that Culp inherited in October 2018 was a company in crisis. Jack Welch had turned it into a sprawling financial and industrial machine: mortgages, credit cards, jet engines, NBC, medical imaging. For a decade it worked. At its peak in 2000, GE’s market capitalisation approached $600 billion.

Then it stopped working. Jeff Immelt’s tenure produced a string of missteps, most visibly the $10 billion acquisition of Alstom’s power business in 2015, which landed GE with heavy legacy liabilities and a market that was rapidly moving against large gas turbines. GE Capital, designated systemically important by US regulators, consumed capital and generated risk at a scale that made the business unmanageable. By 2018, GE’s total debt load had exceeded $90 billion, the quarterly dividend had been cut to a penny per share, and the company was removed from the Dow Jones Industrial Average, where it had been a member, with interruptions, since 1896.

John Flannery replaced Immelt in 2017 and lasted barely a year. Culp, who ran Danaher for 14 years and built a reputation for lean manufacturing discipline, joined GE’s board in May 2018 and became CEO that October. He was the first external CEO in GE’s history.

His first move was to stop the bleeding. The plan to spin off GE Healthcare was shelved; the business was too important a source of cash to give up while the debt crisis was unresolved. Culp sold the biopharma unit, which makes equipment and materials used to manufacture drugs, to his former employer Danaher for $21.4 billion in early 2020. The deal closed a week before COVID shutdowns began. In 2021, GE merged its aircraft leasing arm (GECAS) with Ireland’s AerCap in a transaction valued at $31 billion, reducing debt by approximately $30 billion. GE Transportation was merged with Wabtec. By the time Culp was ready to execute the full break-up, GE was a solvent company again.

He named the break-up plan Project Revere, after a monument near his Boston home. In November 2021, a week after the AerCap deal closed, GE announced it would split into three independent public companies. GE Healthcare completed its spin-off in January 2023. GE Vernova followed on April 2, 2024, with Scott Strazik, who had led the power business since 2020, named CEO. GE itself continued as GE Aerospace.

What GE Vernova actually sells

The company launched with approximately 85,000 employees across more than 100 countries. By year-end 2024, restructuring had reduced that figure to approximately 77,000, where it remained through 2025. It operates major manufacturing facilities in Greenville, South Carolina (gas turbines), Belfort, France (steam and gas equipment), and Schenectady, New York (electrical equipment and generators). GE Vernova launched debt-free with $3.6 billion in cash. Cash grew to $8.8 billion by year-end 2025, even after $3.6 billion in shareholder returns through dividends and buybacks.

The three business segments tell different stories.

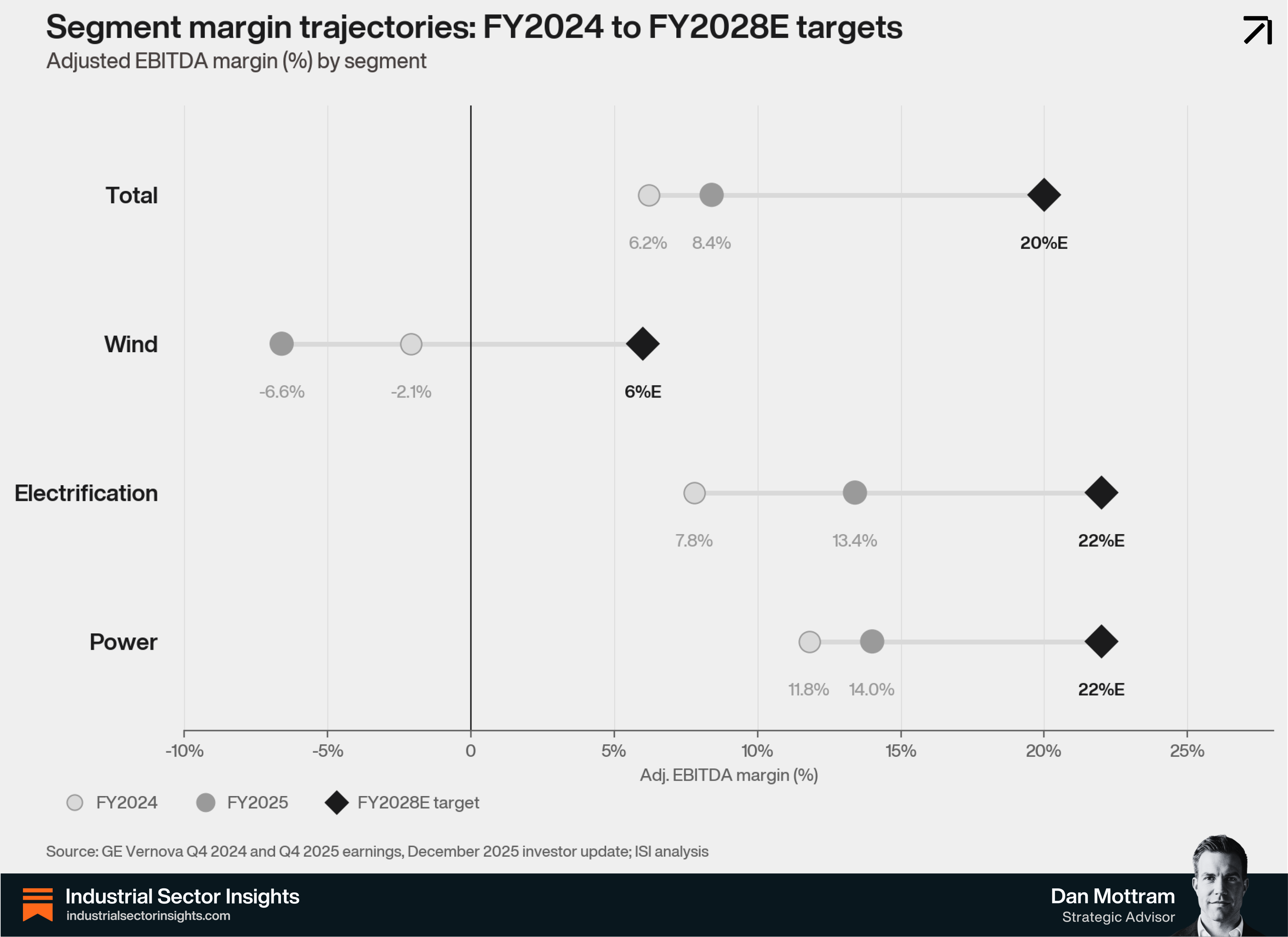

Power is the stable core and earnings engine. Gas Power accounts for the bulk of it, built on an installed base of approximately 7,000 gas turbines globally. The flagship product, the HA turbine platform, has become the standard for high-efficiency combined cycle generation. By early 2025, GE Vernova had commissioned more than 115 HA units, logging over 3 million operating hours across 53 GW of installed capacity.

Power orders hit $32.8 billion in 2025, up 52 per cent organically, driven by the accelerating build-out of data centre infrastructure and utilities locking in long-cycle capacity ahead of projected demand. In Q4 2025 alone, GE Vernova signed 24 GW of new gas equipment contracts, including 21 GW of slot reservation agreements and 3 GW of firm orders. The gas turbine backlog stood at 83 GW at year-end, with management targeting 100 GW by end of 2026. Pricing in slot reservation agreements is running 10 to 20 points stronger than prior cycle levels. Segment EBITDA margin expanded 220 basis points year-over-year. Nuclear remains a smaller Power contributor. The BWRX-300 small modular reactor is under construction at Darlington, Ontario, with completion targeted for end-2029 and operation by 2030.

Wind is the turnaround story that has yet to arrive. Segment revenue fell to $9.1 billion from $9.7 billion. EBITDA losses hit $600 million, well above the $200-400 million guidance. The overrun reflected additional costs from the US government’s stop-work order on the Vineyard Wind project and ongoing losses in offshore wind. Q4 2025 Wind revenue fell 25 per cent quarter-on-quarter, driven by lower onshore equipment deliveries. For 2026, management is guiding for Wind revenue to decline again in the low double digits, with EBITDA losses of approximately $400 million. Onshore wind is closer to breakeven. Offshore remains firmly in the red.

Electrification is where the market has most aggressively re-rated the stock. Revenue grew 26 per cent in 2025 to $9.6 billion, and EBITDA margin expanded by 560 basis points, reflecting strong pricing power and operating leverage as volume grew. Equipment backlog reached $30.5 billion by year-end, up 53 per cent. In Q4, Electrification orders ran at approximately 2.5 times revenue, meaning the segment is building backlog faster than it is deploying it. Grid equipment demand, including switchgear, substations, and synchronous condensers, continues to outrun available supply capacity.

The segment’s growth accelerated further with the acquisition of the remaining 50 per cent stake in Prolec GE, the company’s transformer joint venture in Mexico, from Xignux for $5.275 billion. Announced in October 2025 and closed in February 2026, the deal consolidates control over a product line that faces three-year delivery lead times in some markets. Prolec GE should contribute roughly $3 billion to Electrification revenue in 2026.

Why the competitive position is harder to replicate than it looks

Three companies dominate the global large gas turbine market: GE Vernova, Siemens Energy, and Mitsubishi Power. Combined, they hold the vast majority of the installed base. The concentration reflects the barriers to building a competitive gas turbine business from scratch.

Development lead times run to decades. A new turbine design requires thousands of hours of testing, materials science that has been refined over multiple product generations, and a service network capable of maintaining equipment across the full 30-to-40-year asset life. The HA platform’s 3 million-plus operating hours give GE Vernova a data advantage that a new entrant cannot replicate. Customers running baseload gas generation do not experiment with unproven suppliers. Pricing data from 2025 slot agreements confirms incumbents can raise prices without losing orders.

The service and aftermarket revenue stream compounds this advantage. Every turbine sold creates a long-term service relationship. The installed base of 7,000 turbines generates recurring revenues through maintenance, parts, and upgrades. That base is growing, and the upgrade cycle is accelerating as older, less efficient units are pushed harder to meet rising demand. Services account for more than 55 per cent of backlog, ensuring multi-year earnings visibility.

The Electrification segment benefits from similar structural constraints. Grid transformers and switchgear are not commodities. Delivery lead times for high-voltage transformers now extend to three years in some markets. GE Vernova’s manufacturing capacity and existing utility relationships position it ahead of new entrants in a supply-constrained environment. The Prolec GE acquisition, priced at $5.3 billion, reflects what full control of a constrained manufacturing asset is worth in this cycle.

The offshore wind problem

The company’s offshore wind business had a worse 2025 than its top-line numbers suggest. Three Haliade-X blade failures in the second half of 2024 continued to affect operations and costs into 2025, and the Trump administration’s early decision to halt new offshore wind permitting effectively closed the US pipeline for future projects.

The first failure occurred at Dogger Bank A off England in May 2024, attributed to an installation error. The second, more damaging incident occurred on July 13, 2024, at Vineyard Wind 1 off Nantucket, Massachusetts. GE Vernova’s investigation traced it to a manufacturing deviation at its LM Wind facility in Gaspé, Quebec, specifically insufficient bonding of blade components. A Reuters investigation found managers pushed workers to increase output, compromising quality control. The company laid off nine managers and suspended 11 floor workers. In July 2025, GE Vernova settled with the Town of Nantucket for $10.5 million, establishing a Community Claims Fund to compensate local businesses. The third failure, at Dogger Bank A again on August 22, 2024, was caused by a commissioning error: the turbine had been left in a fixed, static position during high winds, a distinction GE Vernova made explicitly because it pointed away from a design flaw.

Into 2025, the US government’s stop-work order on Vineyard Wind added costs the company had not fully anticipated. The project remains behind schedule. The administration’s pause on new offshore permitting has halted any US projects not already under construction. The onshore wind market is closer to recovery. Offshore remains a drag that the company has stopped trying to characterise as temporary.

The broader offshore wind sector difficulties extend across the industry. Project cancellations, cost inflation, and supply chain constraints have affected Siemens Gamesa and Vestas as well. GE Vernova’s 2025 results confirm that Wind losses will carry into 2026, the segment will decline in revenue terms, and the offshore component remains the primary pressure point.

The trajectory

GE Vernova’s 2025 results showed what the company looks like when Power and Electrification are running well and Wind has yet to be fixed. Revenue grew 9 per cent to $38.1 billion. Adjusted EBITDA reached $3.2 billion, with margin expanding 210 basis points to 8.4 per cent. Free cash flow more than doubled to $3.7 billion from $1.8 billion in 2024. The cash balance ended the year at $8.8 billion. Net income was $4.9 billion, though that includes a $2.9 billion tax benefit from a US valuation allowance release. EBITDA better reflects underlying operations.

The $150 billion backlog is the most important number.

It grew $31.2 billion during 2025 alone. Equipment margins expanded six points year-over-year, meaning new contracts price better than current work. Power held $83 GW of gas turbine backlog at year-end. Electrification’s equipment backlog reached $30.5 billion. Services represent more than half of the total, providing multi-year earnings visibility at a scale that few industrial manufacturers can match.

For 2026, GE Vernova is guiding for revenue of $44-45 billion (incorporating Prolec GE), adjusted EBITDA margin of 11-13 per cent, and free cash flow of $5.0-5.5 billion. The 2028 targets are more ambitious: $56 billion in revenue, 20 per cent EBITDA margin, and $24 billion-plus in cumulative free cash flow. Management pegs those targets to a backlog approaching $200 billion by end-2028.

The question at current valuations: Can Power and Electrification compound at guided rates while Wind losses stay contained?

Gas turbine demand is structurally supported by data centre load growth, baseload reliability requirements, and the long-cycle nature of utility contracts. Electrification order growth at 2.5 times revenue signals sustained grid equipment demand. The constraint is whether GE Vernova can scale manufacturing fast enough to convert backlog into revenue without margin erosion. The company has committed to investing $6 billion in capital expenditure between 2025 and 2028.

At $846 in February 2026, the stock prices in substantial good news. Whether it is worth that price is a different question from whether the business is well-positioned.

On the business, the evidence from 2025 is clear: Power and Electrification are executing, the backlog is growing faster than revenue, and pricing is strengthening.

On the stock, the 2028 targets would need to be largely met at margins the company has not yet demonstrated to justify the current multiple.

The Wind drag is a known, quantified risk.

The execution risk, converting $150 billion of backlog into cash, is the variable that matters now.